Counterpoint Research is attending 5G Summit & Analyst Conference 2023

Our Associate Director, Gareth Owen will be attending the 5G Summit & Analyst Conference 2023 at Bangkok, Thailand. You can schedule a meeting with him to discuss the latest trends in the technology, media and telecommunication sector and understand how our leading research and services can help your business.

When: 14th & 15th November 2023

Where: Bangkok, Thailand

About the event:

The 5G Summit & Analyst Conference aims to bring together a gathering of influential thought leaders, pioneers, and like-minded individuals who share a passion for harnessing the potential to shape a brighter future. The theme for this year is ‘Embrace the Digital Nexus’.

Click here (or send us an email at contact@counterpointresearch.com) to schedule a meeting with them.

In some markets, operators await evidence of successful use cases before switching to 5G SA.

In H1 2023, the Asia-Pacific region continued to lead in terms of 5G SA Core deployments.

Ericsson led the overall market followed by Nokia, Huawei, ZTE, Samsung, and Mavenir.

Counterpoint Research’s recently published July update of the 5G SA Core Tracker is a culmination of an extensive study of the 5G SA market. It provides details of all operators with 5G SA cores in commercial operation at the end of H1 2023, including market share by region, vendor, and the popular frequency bands for deployments. Apart from that, it touches upon the potential monetization opportunities for telecom operators across different domains and uses cases.

Last year, there was steady growth in the commercial deployment of 5G Standalone (SA), with more than 20 operators moving to 5G standalone core. However, the pace slowed down in H1 2023 with the number of operators launching commercial 5G SA ranging in single digits. The primary reason for the slowdown in commercial deployment of 5G SA was the restraint arising from global macroeconomic factors and the lack of a clear picture of 5G monetization for operators. Although the pace of commercial deployment has slowed down in 2023, operators are working on monetization avenues, and are working on SA-specific use cases, including on-demand network slicing and FWA.

Most of the 5G SA commercial deployments have been in developed economies, and Counterpoint Research expects the next bulk of network rollouts will take place in emerging markets. This will drive the continuing transition from 5G NSA to 5G SA.

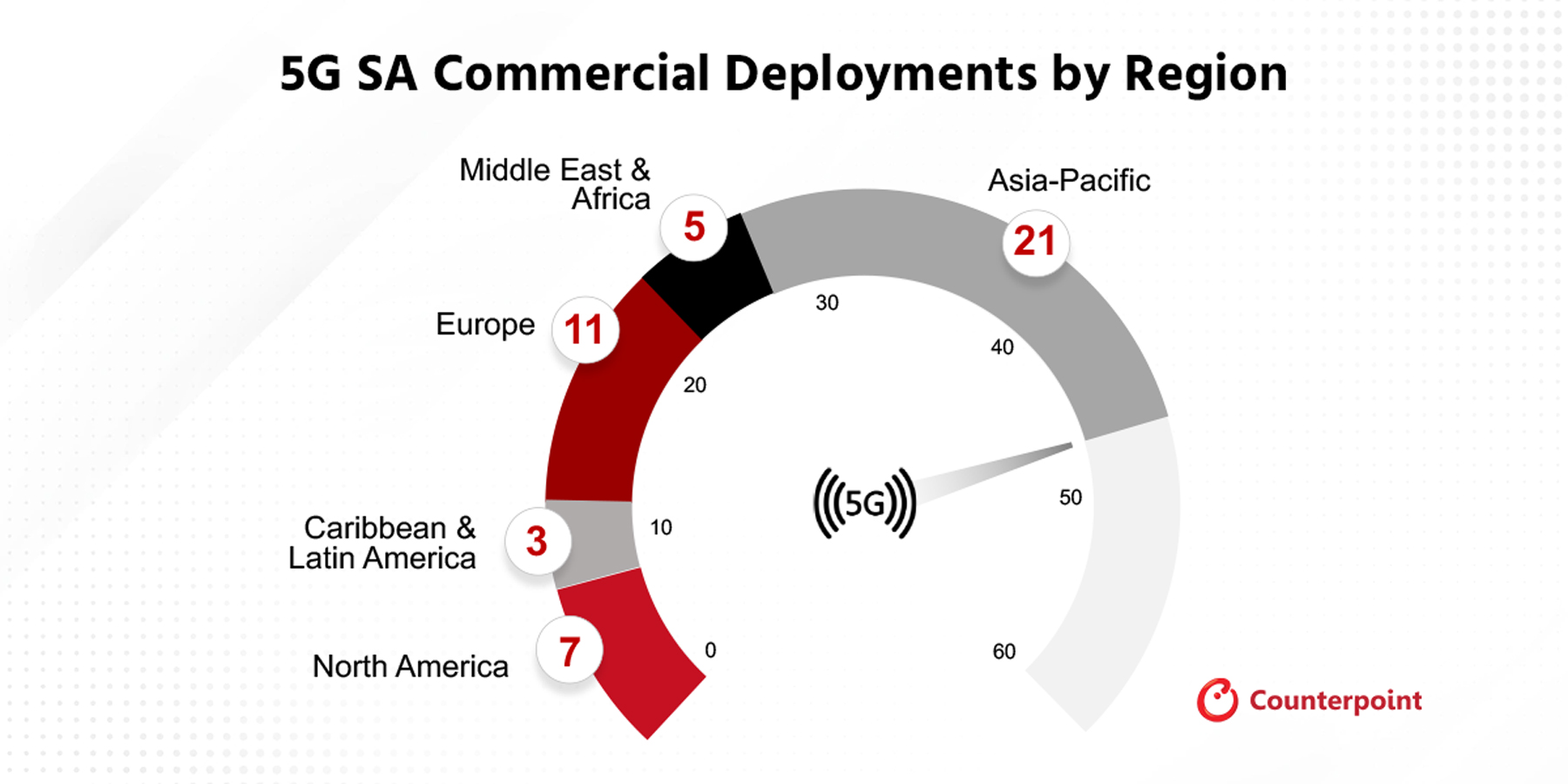

Exhibit 1: 5G SA Deployments by Region, H1 2023

As shown in Exhibit 1, the Asia-Pacific region led the segment, followed by Europe and North America, with the other regions – Middle East and Africa, and Latin America – lagging.

Key Points

Key points discussed in the report include:

Operators – 47 operators have deployed 5G SA commercially with many more in the testing and trial phase. Globally, most of the deployments are in developed economies with those in emerging economies lagging. Although the pace of deployment is steady in developed markets, it is progressing slowly in emerging markets, and in some markets, operators are biding their time and looking for evidence of successful use cases before switching from 5G NSA to SA. The ongoing economic headwinds also delayed the commercial deployment of SA, which was seen in H1 2023.

Vendors – Ericsson and Nokia lead the 5G SA Core market globally and are benefiting from the geopolitical sanctions on Chinese vendors Huawei and ZTE in some markets. South Korea’s Samsung and Japan’s NEC are mainly focused on their respective domestic markets but are expanding their reach to Tier-2 operators and emerging markets, while emerging vendors Parallel Wireless and Mavenir are working with leading operators in Europe, and Middle East and Africa.

Spectrum – Most operators are deploying 5G in mid-band frequencies, n78, as it provides faster speeds and good coverage. Some operators have also launched commercial services in the sub-GHz n28 and mmWave wave n258 bands. FWA seems to be the most popular use case at present but there is a lot of interest in edge services and network slicing as well.

Use Cases – Operators are looking for avenues to monetize the 5G services, as they are struggling to make the RoI from their investments in 5G. Although FWA is a promised application for 5G SA monetization, there are many other use cases that operators can look into to increase their RoI, including network slicing, live broadcasting, XR applications, and private networks. Although eMBB is the most widely used 5G use case currently, MNOs need to move to 5G SA to leverage URLLC and mMTC use cases.

Report Overview

Counterpoint Research’s 5G SA Core Tracker, July 2023 provides an overview of the 5G Standalone (SA) market, highlighting the key trends and drivers that are shaping the market, along with details of commercial launches by vendor, region, and frequency band. Additionally, the tracker provides details about the 5G SA vendor ecosystem split into two categories – public operator and private network markets.

Table of Contents:

Overview

Market Update

5G SA Market Deployments

Commercial Deployment by Operators

Network Engagements by Region

Network Engagements by Deployments Status

Leading 5G Core Vendors

Mobile Core Vendor Ecosystem

5G Core Vendors Market Landscape

Outlook

5G Standalone Use Cases

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Apple and Samsung shipped 26% and 14% more smartphones YoY amid market declines.

HONOR rose 200% YoY driven by its multi-channel and multi-device strategy.

ZTE rose 50% YoY due to its low-price-band portfolio and increasing spots in the open channel.

Bogota, Buenos Aires, New Delhi, Hong Kong, Seoul, London, Beijing, San Diego – March 13, 2023

Colombia’s smartphone shipments fell 3% YoY in 2022, according to the latest research from Counterpoint’s Market Monitor service. OEMs recorded mixed numbers, ranging from rising stars like HONOR with a 200% YoY growth to incumbents like HMD with double-digit declines of more than 40%.

Principal Analyst Tina Lu said, “Like the rest of the region, Colombia is being affected by macroeconomic headwinds, just a bit more due to the risks connected with the new government. It has decreased the number of VAT-free days, which used to be the main events for driving sales. But still, the shipment decline was much less compared to LATAM’s 5.5% YoY fall. This is because Colombia’s market finished the year with a higher level of inventory.”

Research Analyst Andres Silva said, “Inventory was the biggest worry of OEMs in 2022. Samsung, Apple and ZTE grew in double digits in 2022, reflecting the importance of tried and tested channel management processes in the country. Also, brand equity plays a key role – with economic uncertainty, consumers tend to prefer known brands. Motorola and Xiaomi suffered specifically in the premium and flagship devices. Even local kings, or the ‘Others’ category, shipped 8% less YoY.”

Commenting on the overall market outlook, Silva said, “Going forward, the market might continue to decline as end users are showing more appetite for experiences. For example, concerts and outdoor activities increased 37% YoY in 2022, the second year of post-COVID reopening. The replacement cycle continues to lengthen while shipment units recover to pre-pandemic levels. Nevertheless, the market still has room to grow – sub-$200 5G devices can become popular if the 5G network rollout picks up.”

Colombia Smartphone Shipment Share, 2021 vs 2022

Source: Counterpoint Research Q4 2022 Market Monitor

Note: Figures may not add up to 100% due to rounding

2022 full-year market summary

Despite the seasonality associated with Q4, which is usually the strongest quarter of the year due to Black Friday and the Christmas holiday season, Q4 2022 could not avoid the 2022 trend of a decrease in consumer demand.

Inflation eased and the peso’s position improved slightly towards the end of Q4, but still, they could not compensate for the purchasing power lost throughout the year.

Samsung grew 14% YoY, with its H2 2022 being better than H2 2021 (+27% YoY). Supply chain constraints were encountered by the OEM in 2021. Also, the Buds 2 bundle offer attracted upgraders and new customers throughout the year.

Motorola declined 38% YoY, with high inventory levels of the Edge 30 series in the operator channel and of the G60 and G60s series in the open channel.

Xiaomi dropped 10% YoY on premium device stocks at stores and the last legs of the Redmi Note 11 series, which slipped drastically in Q4 2022.

ZTE’s shipments increased 50% YoY benefiting from the demand in low-mid and low segments, which are exempt from VAT. Also, ZTE offered device insurance on purchases through the open channel.

Apple was up 26% YoY despite restrictions on its 5G devices following Ericsson’s case against the brand over 5G patent infringement. The iPhone 11, a 4G device, was the OEM’s top-selling model.

TECNO saw another year without a trace of presence in the operator channel. The double-digit YoY loss reflects its lack of exposure to most customers.

HONOR registered the biggest growth of the year at 200% YoY. A multi-channel and multi-device strategy paid off for the brand. The OEM is on track to build brand appeal among Colombians.

OPPO grew 11% YoY driven by in-store marketing activities like an extra warranty (one year more than competitors) on its devices.

vivo’s bet on the FIFA World Cup did not bring results as Colombians failed to find in retail the devices it was promoting.

The ‘Others’ category, mainly composed of local kings, saw an 8% YoY decline. This category’s performance is highly correlated to economic health.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

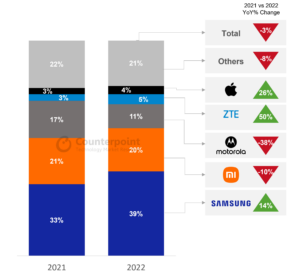

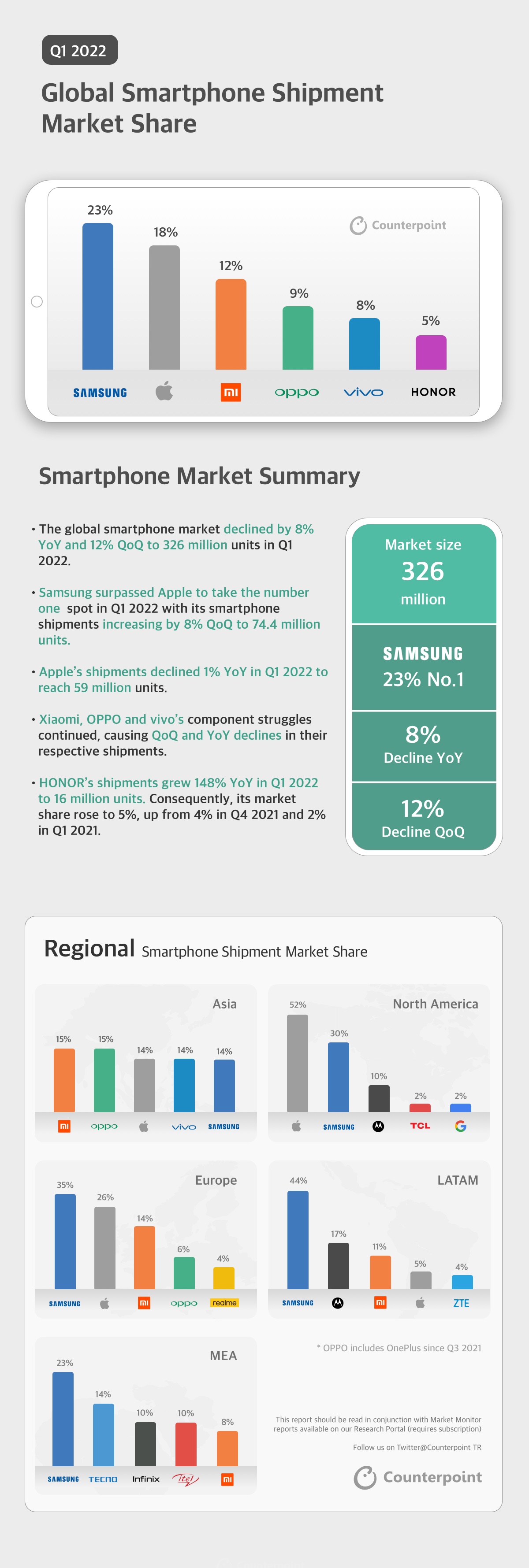

Our Q1 2022 Market Monitor report has been published. We release one infographic each quarter to summarize the smartphone market activities in a single page.

Some quick observations on the smartphone market:

The global smartphone market declined by 8% YoY and 12% QoQ to 326 million units in Q1 2022.

Samsung surpassed Apple to take the number one spot in Q1 2022 with its smartphone shipments increasing by 8% QoQ to 74.4 million units.

Apple’s shipments declined 1% YoY in Q1 2022 to reach 59 million units.

Xiaomi, OPPO and vivo’s component struggles continued, causing QoQ and YoY declines in their respective shipments.

HONOR’s shipments grew 148% YoY in Q1 2022 to 16 million units. Consequently, its market share rose to 5%, up from 4% in Q4 2021 and 2% in Q1 2021.

Use the button below to download the high resolution PDF of the infographic:

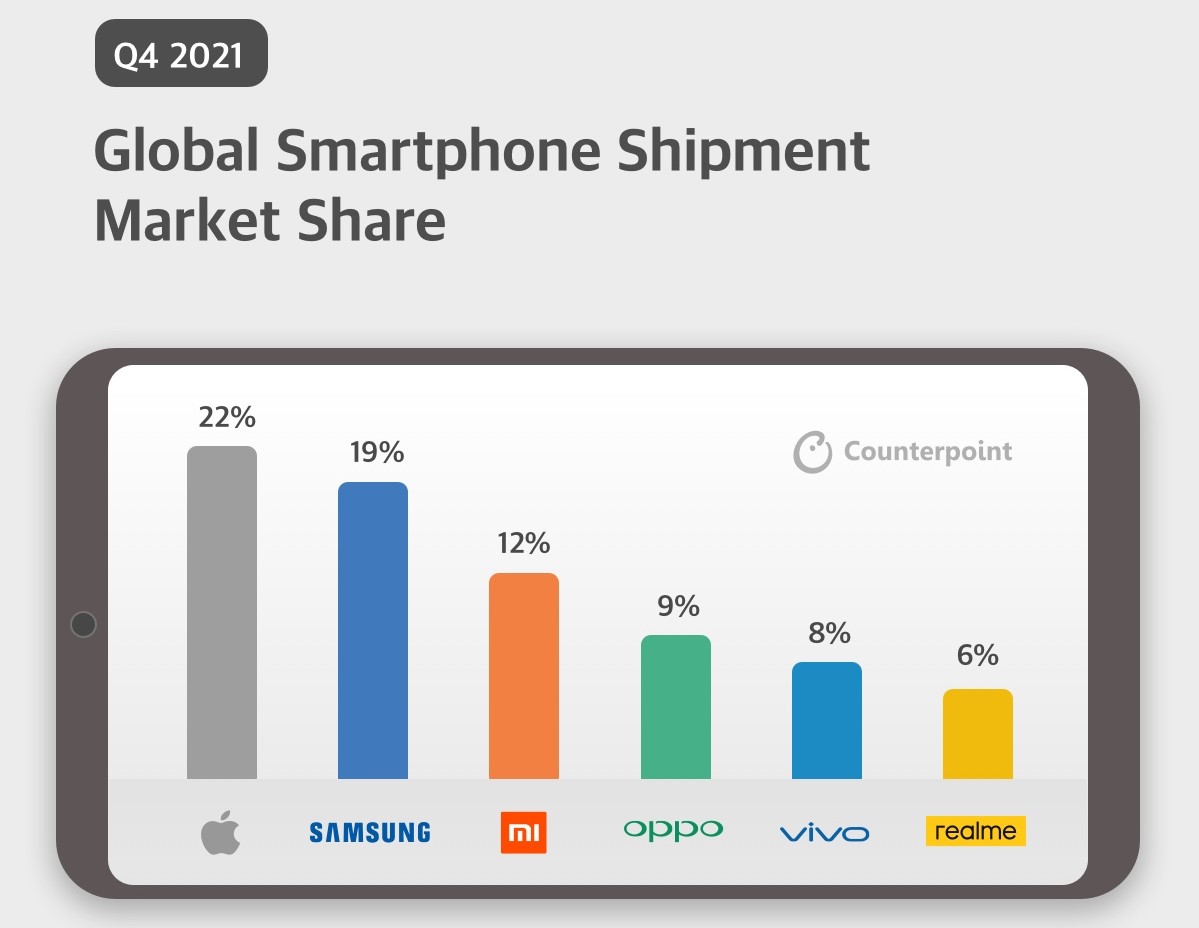

Our Q4 2021 Market Monitor report has been published. We release one infographic each quarter to summarize the smartphone market activities in a single page.

Some quick observations on the smartphone market:

The global smartphone market grew 9% QoQ but declined 6% YoY in Q4 2021, clocking shipments of 371 million units, down from 396 million in Q4 2020.

Apple surpassed Samsung to become the top smartphone vendor in Q4 2021, shipping 81.5 million units.

Xiaomi shipped 45 million units in Q4 2021, up 5% YoY. It grew marginally despite facing severe component shortages.

Samsung shipped 69 million units in Q4 2021, up 10% from Q4 2020, mainly due to increased demand for its smartphones from mid-tier A and M series.

vivo declined 12% YoY to 29.3 million units in Q4 2021 with its market share reaching 8%. Notably, vivo lost the number one spot to Apple in China in Q4 2021.

Use the button below to download the high resolution PDF of the infographic:

London, Hong Kong, Boston, Toronto, New Delhi, Beijing, Taipei, Seoul – February 23, 2022

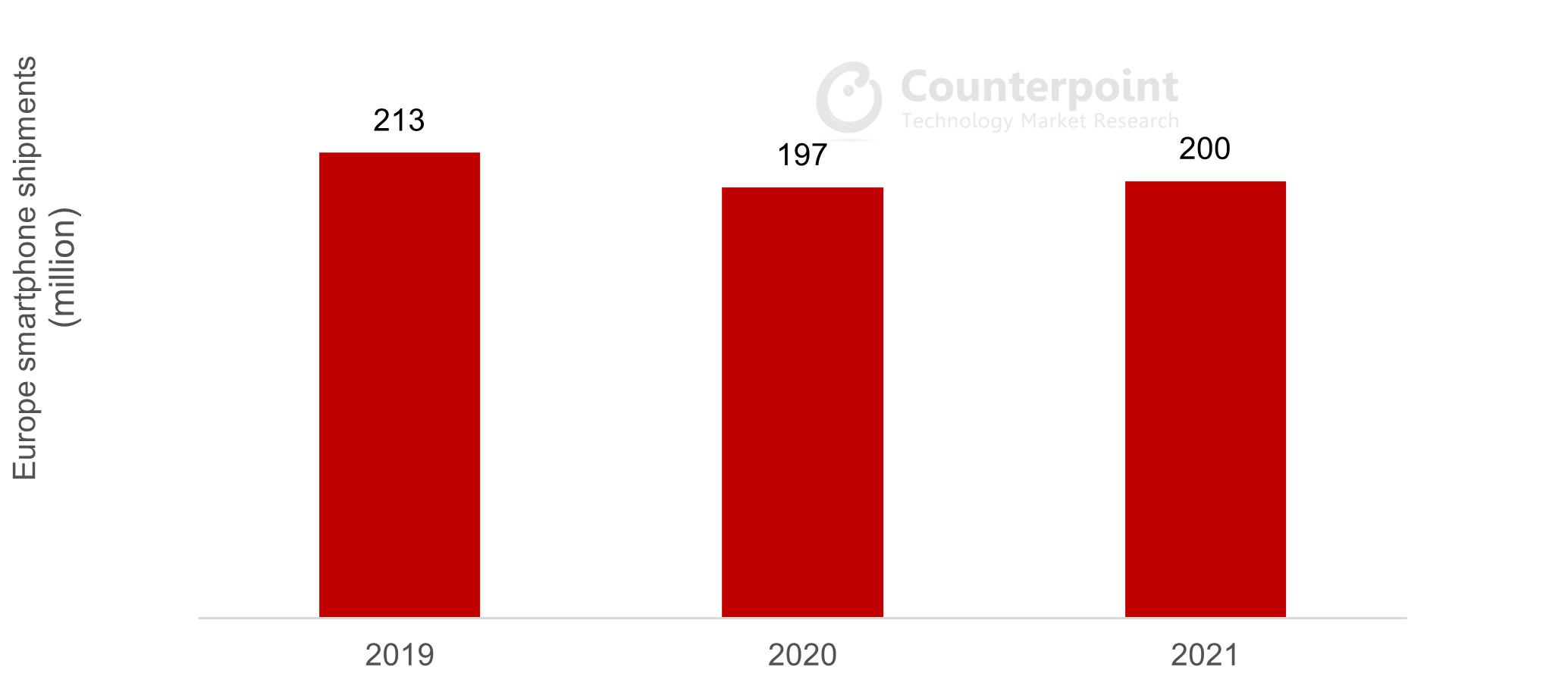

The European smartphone market is slowly on the road to recovery. With the end of the COVID-19 pandemic seemingly in sight, and despite new challenges around component shortages, the market registered a 1% annual rise in smartphone shipments in 2021, a reversal of the 7% annual decline recorded in 2020.

This modest growth, while a positive sign, is nevertheless a reminder that the region’s smartphone market is still not back to full strength, with shipments well below 2019 levels. Having said that, some vendors certainly had a year to celebrate.

Europe smartphone market rebounded in 2021 after a difficult 2020

Source: Counterpoint Research Market Monitor Q4 2021

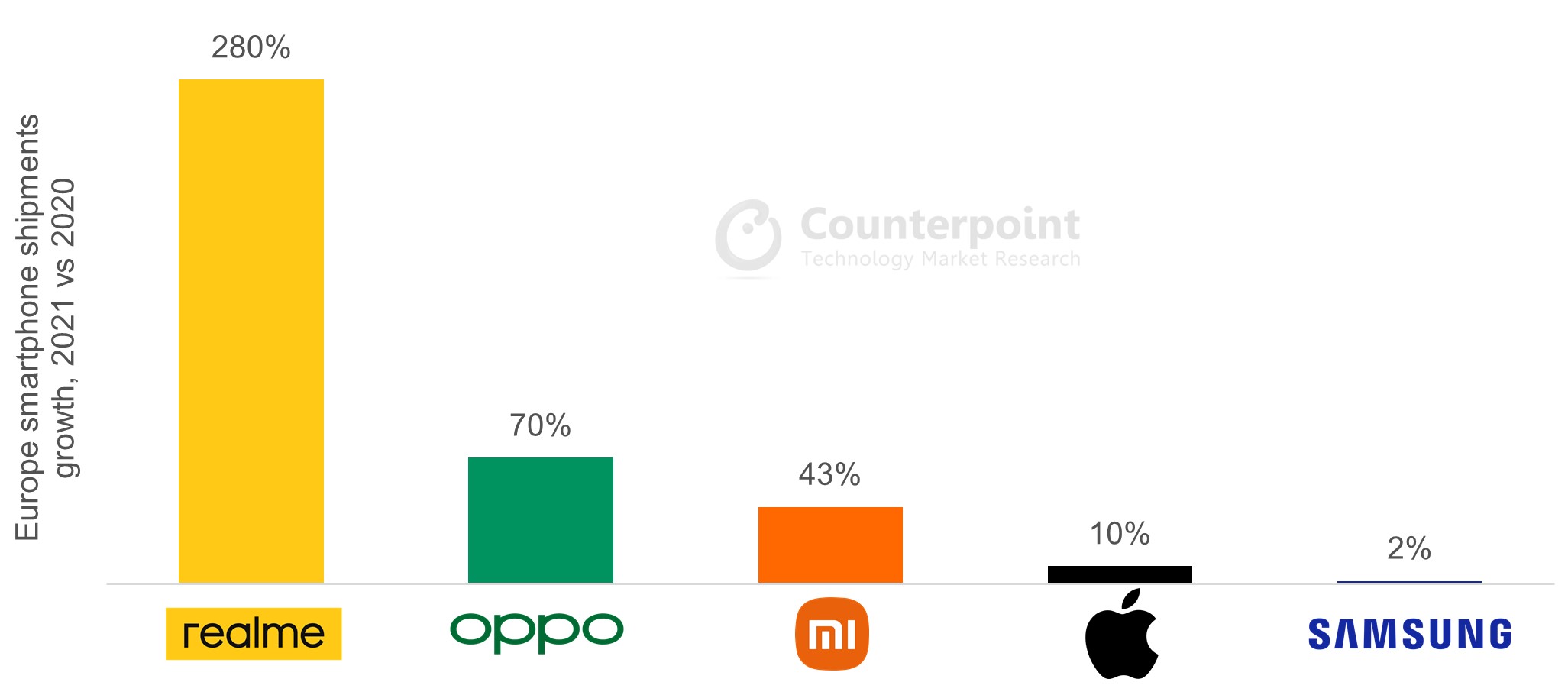

Counterpoint Research’s Associate Director, Jan Stryjak said “given the difficulties – both supply- and demand-side – that vendors faced in 2020, it is unsurprising that most posted good growth in Europe in 2021. The pick of the bunch, however, was realme, which had its best year since entering the region and was, by a fair margin, the fastest growing major brand in Europe in 2021. realme has gone from strength to strength in Europe. It entered the market in June 2019 and quickly found favour with its ‘flagship killer’ approach, offering high-spec devices at competitive prices.”

realme’s shipments grew six-fold in 2020 compared to 2019, and realme succeeded in building a European base with its affordable devices, especially in Eastern Europe (most notably Poland and the Czech Republic) and price-conscious Western European markets such as Italy, Greece and Spain.

The success of realme GT series and Number series helped drive realme to new heights in Europe, with 280% annual growth in 2021 as the fastest growing smartphone brand in Europe, overtaking OPPO (70% annual growth in 2021), Xiaomi (43%), Apple (10%) and Samsung (2%).

realme is the fastest growing brand in Europe

Source: Counterpoint Research Market Monitor Q4 2021 Note: Xiaomi includes Redmi and POCO, OPPO includes OnePlus

Its growth in the last year means realme has established itself as a top five vendor in Europe, climbing five places in 2021 by overtaking Wiko, Motorola, Alcatel, HONOR and Huawei. And things could get even better: realme saw a significant jump in shipments in Europe in Q4 2021, accounting for just under 6% of the region’s total smartphone shipments (up from 2.5% in Q3 2021). So, the trajectory is looking very promising for realme.

realme climbed five places in 2021

Source: Counterpoint Research Market Monitor Q4 2021. Ranking based on annual Europe smartphone shipments. Note: Xiaomi includes Redmi and POCO, OPPO includes OnePlus

Speaking about realme’s short-term strategy, Counterpoint Research’s Senior Analyst, Harmeet Singh Walia said “having established itself as a key affordable brand in Europe, realme’s next goal is to increase its profit margins by further pushing premium devices. The upcoming launch of its GT2 series at MWC22 is a step in this direction, helping boost realme’s differentiation, brand equity and a halo effect to attract users looking to upgrade to high-tier or entry premium-tier devices. Its challenge will be to convince customers who are used to purchasing from established brands, and in this regard, Europe is a tough nut to crack. realme will be up against not just Apple and Samsung, but from fellow Chinese brands like Xiaomi, OPPO and vivo who are all also looking to gain a bigger share of the European pie.”

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Our Q3 2021 Market Monitor report has been published. We release one infographic each quarter to summarize the mobile handset market activities in a single page.

Some quick observations on the smartphone market:

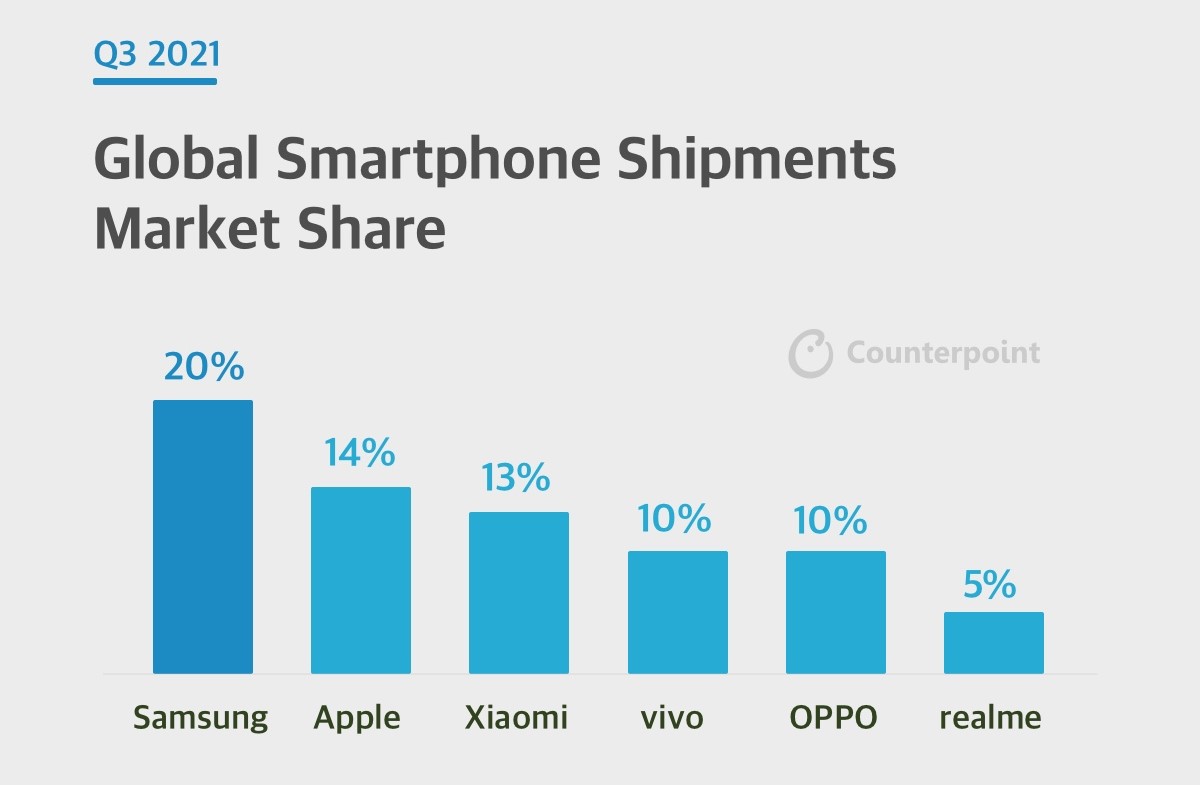

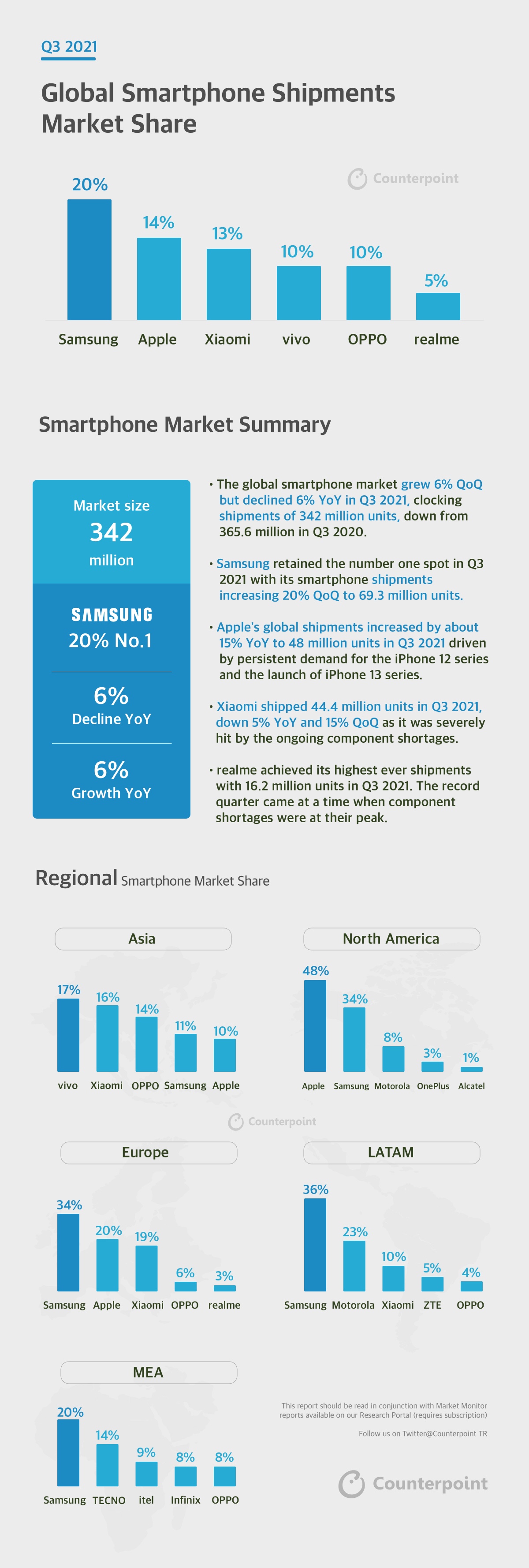

The global smartphone market grew 6% QoQ but declined 6% YoY in Q3 2021, clocking shipments of 342 million units, down from 365.6 million in Q3 2020.

Samsung retained the number one spot in Q3 2021 with its smartphone shipments increasing 20% QoQ to 69.3 million units.

Apple’s global shipments increased by about 15% YoY to 48 million units in Q3 2021 driven by persistent demand for the iPhone 12 series and the launch of iPhone 13 series.

Xiaomi shipped 44.4 million units in Q3 2021, down 5% YoY and 15% QoQ as it was severely hit by the ongoing component shortages.

realme achieved its highest ever shipments with 16.2 million units in Q3 2021. The record quarter came at a time when component shortages were at their peak.

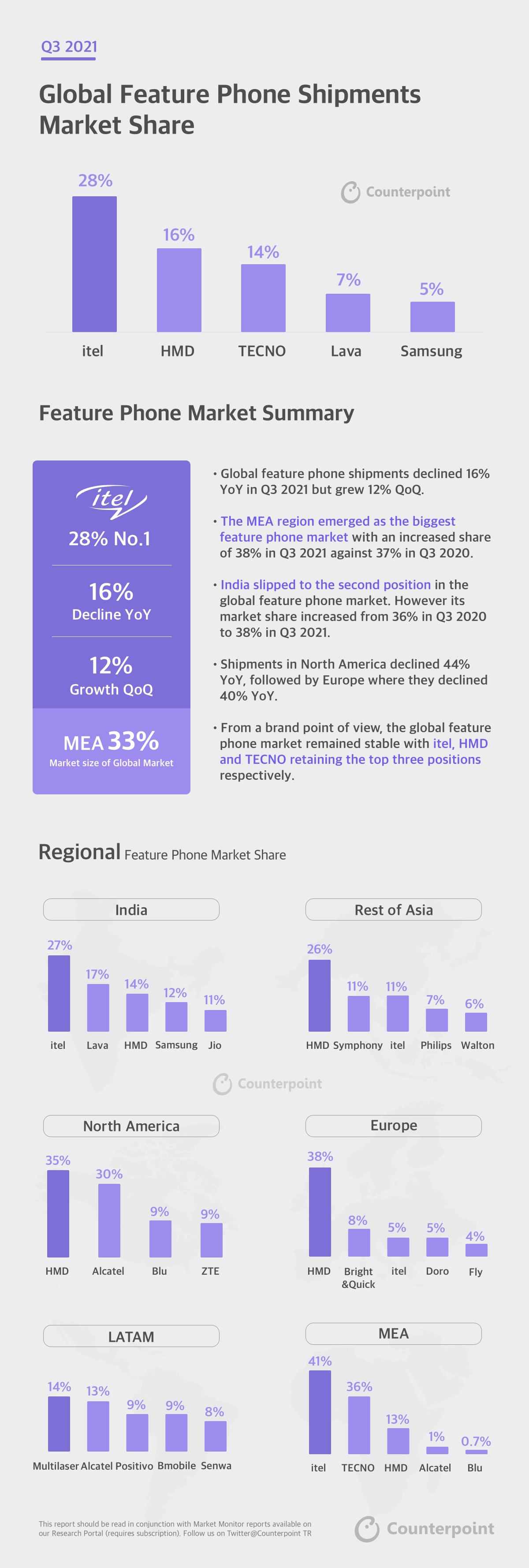

Some quick observations on the feature phone market:

Global feature phone shipments declined 16% YoY in Q3 2021 but grew 12% QoQ.

The MEA region emerged as the biggest feature phone market with an increased share of 38% in Q3 2021 against 37% in Q3 2020.

India slipped to the second position in the global feature phone market. However its market share increased from 36% in Q3 2020 to 38% in Q3 2021.

Shipments in North America declined 44% YoY, followed by Europe where they declined 40% YoY.

From a brand point of view, the global feature phone market remained stable with itel, HMD and TECNO retaining the top three positions respectively.

Use the button below to download the PDF version of the infographic:

Buenos Aires, New Delhi, Hong Kong, Seoul, London, Beijing, San Diego – November 29, 2021

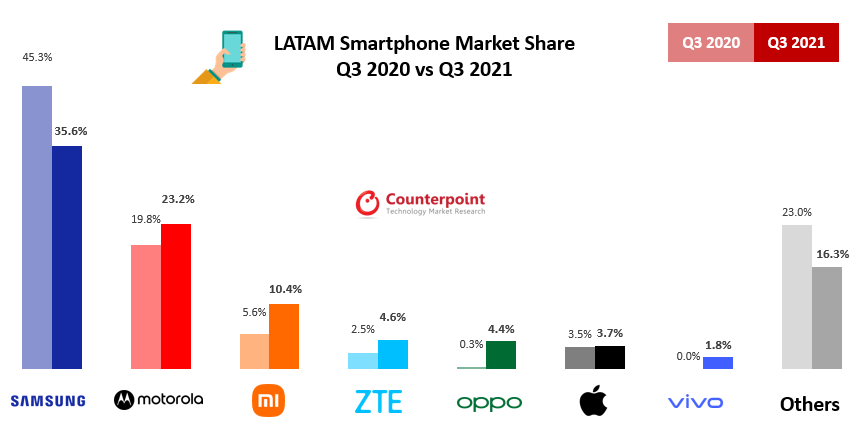

The LATAM smartphone market is heating up with the arrival of more players. In the last year, at least five new brands entered the region. Despite this, the market grew only 0.7% YoY and 3.1% QoQ in Q3 2021, impacted by the ongoing component shortages.

Commenting on the market dynamics, Principal AnalystTina Lu said: “For the past two or three years, LATAM has been a highly concentrated market. New brands entering the market are driving this concentration down a few points. A more open market benefits a consumer by providing more choices at competitive prices. This trend will most likely continue as an increasing number of brands see growth prospects in LATAM. The Brazilian and Argentinian markets are the least open in the region, as they require local manufacturing. Therefore, Brazil’s market was the most affected by the component shortages that impacted the smartphone manufacturing/assembling industry in Q2 2021 and further deepened in Q3 2021.”

Lu added, “Samsung’s shipments were impacted by Brazil and Vietnam factory woes. As a result, its market share reached the lowest in the previous seven quarters. Samsung continued to be the leader in the region, but this volume drop allowed its closest competitor Motorola to narrow the gap. Motorola is improving its product availability in the region. It continued to lead the Mexican market while improving its position in Argentina and Brazil.”

Source: Counterpoint Research Market Monitor, Q3 2021

Commenting on brand performance, Research Analyst Andres Silva said, “OPPO managed to outsell Apple in Q3 2021 to become one of the five top-selling brands in the region. This is the first time that this Chinese OEM, which re-entered LATAM last year, is in the region’s bestseller chart. The brand saw rapid growth in Mexico. OPPO is growing beyond the Mexican market, but it needs to build the branding in these markets, which is more challenging compared to Mexico.”

Market Summary

Samsung dropped almost 10% points in its LATAM share. Its volume decreased in almost every major country in the region except for Argentina and Peru.

Brazil, Mexico, and Argentina were the biggest markets for Samsung in terms of sales volume.

Motorola led the Mexican market and was a strong second in Argentina and Brazil. In all the other LATAM countries, its second position was challenged by Xiaomi.

Xiaomi’s shipments almost doubled YoY. However, its volume dropped compared to the previous quarter. This was the first quarter in the last three years (except the COVID-19-hit Q2 2020) that this Chinese brand saw a QoQ drop.

Xiaomi wants to position itself as the leading 5G brand in LATAM. It launched the Redmi Note 10 5G during the quarter with very aggressive pricing.

Xiaomi is a close leader in Colombia and a strong second player in Chile and Peru. It is focusing on becoming the leader in these three countries.

ZTE almost doubled its volume YoY. Mexico is its biggest market. It is also focusing on growing in Colombia and Peru in the operator channel.

OPPO continued to stay aggressive in Mexico. It has now expanded to Colombia. But here OPPO will have to work on its brand recognition, so it might take longer to make an impact.

Apple’s volume decreased due to seasonality. The iPhone 13 was launched in most of LATAM in October. On the other hand, there were reports of the iPhone 12 facing big shortages.

vivo is aggressively expanding its presence in the region. It is now growing beyond Colombia and Mexico and has officially entered Chile. But it still needs to build its branding in the region.

The “others” category, especially the “Local Kings”, was impacted once again by the ongoing component shortages.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Boston, Toronto, London, New Delhi, Hong Kong, Beijing, Taipei, Seoul – August 19, 2020

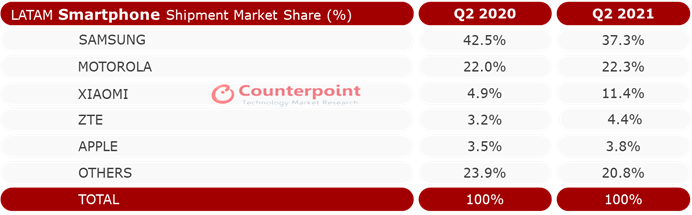

LATAM smartphone shipment increased 41.8% YoY in Q2 2021 but declined 6.5% compared to the previous quarter, according to the latest Market Monitor report from Counterpoint Research. Smartphone demand in the region grew steadily but volume growth was impacted by the ongoing chipset shortages and manufacturing constraints.

The region is still suffering from COVID-19. Only a couple of countries have been able to fully vaccinate more than half of their population. Therefore, most countries are enduring various degrees and forms of lockdown, leading to an economic slowdown. This, in turn, has affected the purchasing ASP (average selling price) rather than the rate of replacement.

Commenting on the market dynamics, Principal AnalystTina Lu said, “LATAM countries’ growth or decline rates varied during the quarter. Brazil was one of the most impacted by component shortages as it has a limited number of brands. On the other hand, Mexico grew compared to the previous quarter, fuelled by fierce competition from new entrants. This led to a larger TAM (Total Addressable Market) in the second biggest market of the region.”

Smartphone Shipment Market Share, Q2 2021

Source: Counterpoint Research Market Monitor, Q2 2021

Lu added, “The volume of most of the brands grew in double or even triple digits YoY. Samsung was the most affected due to the constraints related to its Vietnam factory. Brazilian manufacturing also had supply issues. However, retailers and operators had accumulated some supplies, softening the drop in sell-through. But sell-in was severely impacted. Still, Samsung remains the leading brand in the region, except Mexico and Peru.”

Smartphone Shipment OEM Ranking by Country, Q2 2021

Motorola gained both volume and share in Q2 2021. It capitalized on some of the volume lost by Samsung due to product constraints in the region. In Mexico, it became the market leader. Colombia was the only country that saw a substantial drop in Motorola’s volume affected by Xiaomi. It remains a solid second player in the region.

Xiaomisaw its highest growth ever in the LATAM region. Its volume more than tripled YoY, aided by Huawei’s decline. Xiaomi is now the third-largest player in the region. It has surpassed Samsung to become the number one brand in Peru, the first LATAM country to make it the market leader. In Colombia, it remains slightly below the market leader, Samsung. But Xiaomi’s LATAM growth might slow down due to increasing competition from other Chinese brands.

ZTE volume and share also increased. The brand is increasing its tie-ups with carriers. It benefited from the product supply constraints in the $100 and below segment and LG’s exiting the mobile device market. LG still has some demand, but Samsung, Motorola, ZTE and others are quickly grabbing its volume.

Appledecreased in volume compared to the previous quarter. This is due to the usual seasonality where its sales volume decreases as it gets closer to a new launch. But still, the best-selling model for the American OEM during Q2 2021 was the iPhone 11.

OPPO is the most successful among the Chinese brands that entered the region during the last year or so. However, almost 90% of its volume is concentrated in Mexico. OPPO is placing resources in other LATAM countries, but it still needs to build its branding there. It was in Mexico for a short period in 2017 and is now benefitting from the brand-building undertaken then.

The comprehensive and in-depth Q2 2021 Market Monitor is available for subscribing clients. Feel free to contact us at press(at)counterpointresearch.com for further questions regarding our in-depth research and insights, or for press enquiries.

Background:

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

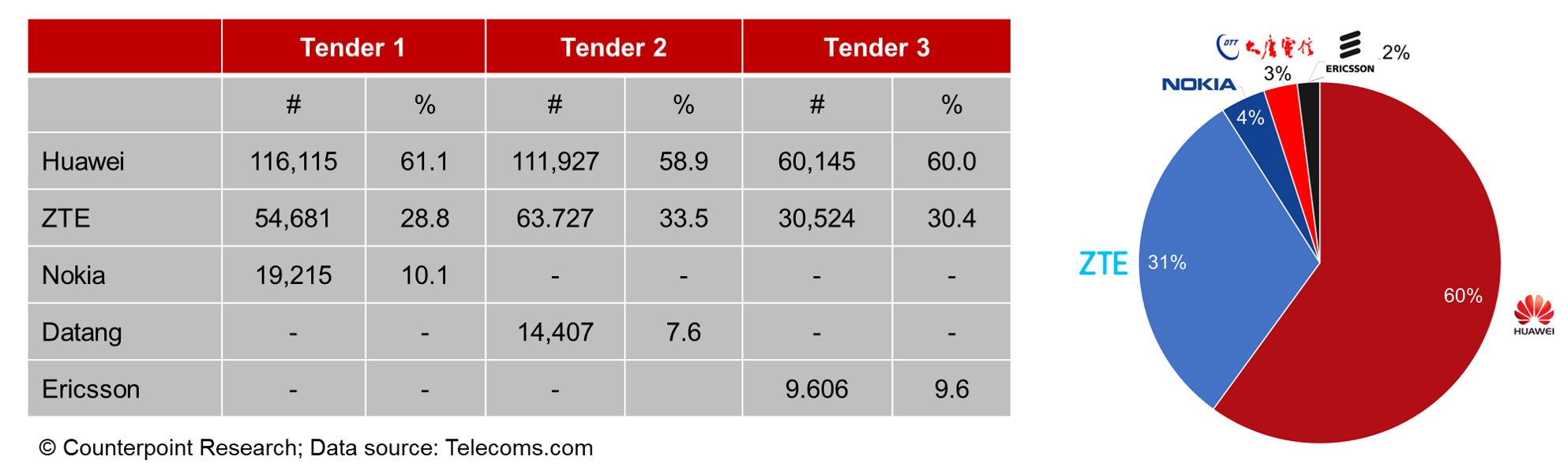

As expected, domestic vendors Huawei and ZTE were awarded the largest contracts in China Broadcasting Network (CBN) and China Mobile’s recent joint 5G infrastructure tenders. Together with compatriot Datang, the trio accounted for 94.1% of the 480,397 base stations under tender with the remaining 6% or 28,822 base stations shared between foreign vendors Ericsson and Nokia (Exhibit 1). Rival operators Chinese Telecom and China Unicom are expected to announce the results of their second 5G tenders in the coming days.

CBN & China Mobile Tender

CBN is the fourth largest operator in China and has partnered with China Mobile to build and operate a 5G network using old analogue TV spectrum in the 700 MHz band. The network is being designed to primarily deliver video streaming services to CBN’s existing cable TV customer base.

Overall, Ericsson was awarded a 2% share of CBN/China Mobile’s three tenders, a not an unexpected result. Clearly, retaliatory measures against Ericsson were inevitable following the Swedish government’s decision to ban Huawei and ZTE from the Swedish 5G market in December 2020. Neighbouring Finland also passed similar legislation but did not specifically mention Huawei or ZTE by name. In the ensuing months, Ericsson has been lowering expectations in China, including warning that it may not be awarded any market share in the current round of tenders. While exclusion cannot yet be ruled out in the China Telecom and China Unicom tenders, it is equally possible that Ericsson could end up with a similar 2% share.

The geopolitical fallout between China and Sweden has also impacted Ericsson’s present 5G contracts in China. In 2019, the company won an 11% share of China Mobile’s first 5G tender. At its second quarter earnings call last week, Ericsson reported a SEK 2.5 billion ($287 million) reduction in revenues in China, a 60% drop Year-on-Year (YoY), due to “lower volumes from delayed 5G deployments.” However, Ericsson claims that this is revenue that has effectively been lost and will not be recouped at a later date.

While China impacted revenues at Ericsson’s Network business, it had a disproportionate knock-on effect on its Digital Services business, where revenues dropped 8% YoY due primarily to lower sales in mainland China. In addition, it was forced to write-off around SEK 300 billion ($34 million) of pre-commercial inventory in China. In contrast, Digital Services showed strong double-digit growth in Europe and North America. However, lower revenues from China coupled with increased R&D investment during the quarter had a negative impact on margins and will now probably push out profitability of Digital Services to 2023.

Nokia Returns to China’s 5G Market

In contrast to Ericsson, Nokia has reasons to celebrate as it is now back in the Chinese 5G RAN market. With a more cost-competitive 5G portfolio compared to 2019, Nokia was awarded a 4% share of the CBN/China Telecom tenders. Although small, it could yet rise in subsequent awards by China Telecom and China Unicom and is an important morale boosting win as the company strives to re-claim global market share.

More importantly, Nokia again has a presence in the Chinese RAN market, a key market for all vendors. Not only is China a volume market, it is also a leader in 5G technology development. It is therefore imperative that vendors have a market presence there. Perhaps a consolation for Ericsson is that it may have avoided the worst scenario – i.e. complete exclusion from the Chinese market.

Ericsson thriving outside China

Despite the setback in China, Ericsson is firing on all cylinders outside China. Revenues at its Networks business unit increased 11% on a constant currency basis, reflecting strong market activity in other regions of the world. Strong growth was reported in Europe as well as in North America, its biggest market, driven by increasing demand for C-band infrastructure. It also won its largest ever contract, a five-year $8 billion contract with Verizon. Ericsson continues to increase its market share, both in markets where it competes against Chinese vendors as well as in markets where they are absent. Counterpoint Research believes that this is largely driven by the steady and continuous improvement in gross margin at the Networks business over the past four years, up from 23% in Q2 2017 to an impressive 47.9% in the most recent quarter.

Geopolitics driving 6G?

Overall, Ericsson’s reduced market presence in China is more than compensated financially by market share gains in other parts of the world, where Chinese vendors are excluded. However, continued geopolitical tensions between China and much of the western world is already starting to have serious implications on the future development of the telecoms industry, particularly with respect to 6G. In recent years, the telecoms industry has benefited from single global 4G/5G standards. Now, a return to the multi-standard days of 3G cannot be excluded.

In order to access

Counterpoint Technology Market Research Limited (Company or We hereafter) Web sites, you may be asked to complete a registration form. You are required to provide contact information which is used to enhance the user experience and determine whether you are a paid subscriber or not.

Personal Information

When you register on we ask you for personal information. We use this information to provide you with the best advice and highest-quality service as well as with offers that we think are relevant to you. We may also contact you regarding a Web site problem or other customer service-related issues. We do not sell, share or rent personal information about you collected on Company Web sites.

How to unsubscribe and Termination

You may request to terminate your account or unsubscribe to any email subscriptions or mailing lists at any time.

In accessing and using this Website, User agrees to comply with all applicable laws and agrees not to take any action that would compromise the security or viability of this Website. The Company may terminate User’s access to this Website at any time for any reason. The terms hereunder regarding Accuracy of Information and Third Party Rights shall survive termination.

Website Content and Copyright

This Website is the property of Counterpoint and is protected by international copyright law and conventions. We grant users the right to access and use the Website, so long as such use is for internal information purposes, and User does not alter, copy, disseminate, redistribute or republish any content or feature of this Website. User acknowledges that access to and use of this Website is subject to these TERMS OF USE and any expanded access or use must be approved in writing by the Company.

– Passwords are for user’s individual use

– Passwords may not be shared with others

– Users may not store documents in shared folders.

– Users may not redistribute documents to non-users unless otherwise stated in their contract terms.

Changes or Updates to the Website

The Company reserves the right to change, update or discontinue any aspect of this Website at any time without notice. Your continued use of the Website after any such change constitutes your agreement to these TERMS OF USE, as modified.

Accuracy of Information:

While the information contained on this Website has been obtained from sources believed to be reliable, We disclaims all warranties as to the accuracy, completeness or adequacy of such information. User assumes sole responsibility for the use it makes of this Website to achieve his/her intended results.

Third Party Links:

This Website may contain links to other third party websites, which are provided as additional resources for the convenience of Users. We do not endorse, sponsor or accept any responsibility for these third party websites, User agrees to direct any concerns relating to these third party websites to the relevant website administrator.

Cookies and Tracking

We may monitor how you use our Web sites. It is used solely for purposes of enabling us to provide you with a personalized Web site experience.

This data may also be used in the aggregate, to identify appropriate product offerings and subscription plans. Cookies may be set in order to identify you and determine your access privileges. Cookies are simply identifiers. You have the ability to delete cookie files from your hard disk drive.

Some quick observations on the feature phone market:

Some quick observations on the feature phone market: